Hinweisgeberschutz

Risikoanalyse und Monitoring

Prüfungen vor Ort

Praktische Handlungs-empfehlungen

Trustnet.Trade Ecosystem

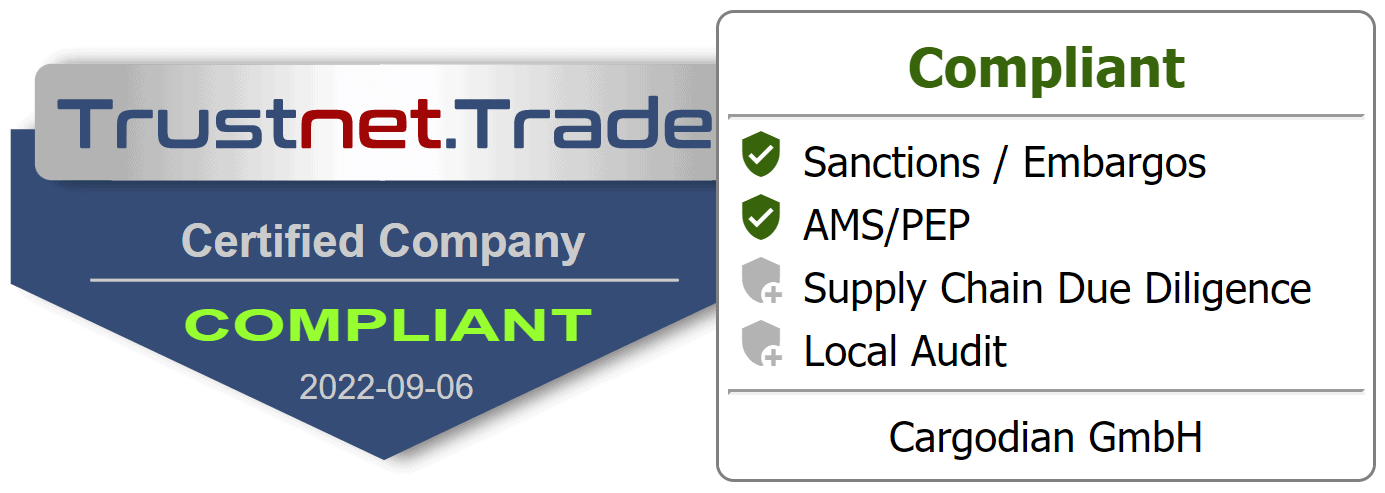

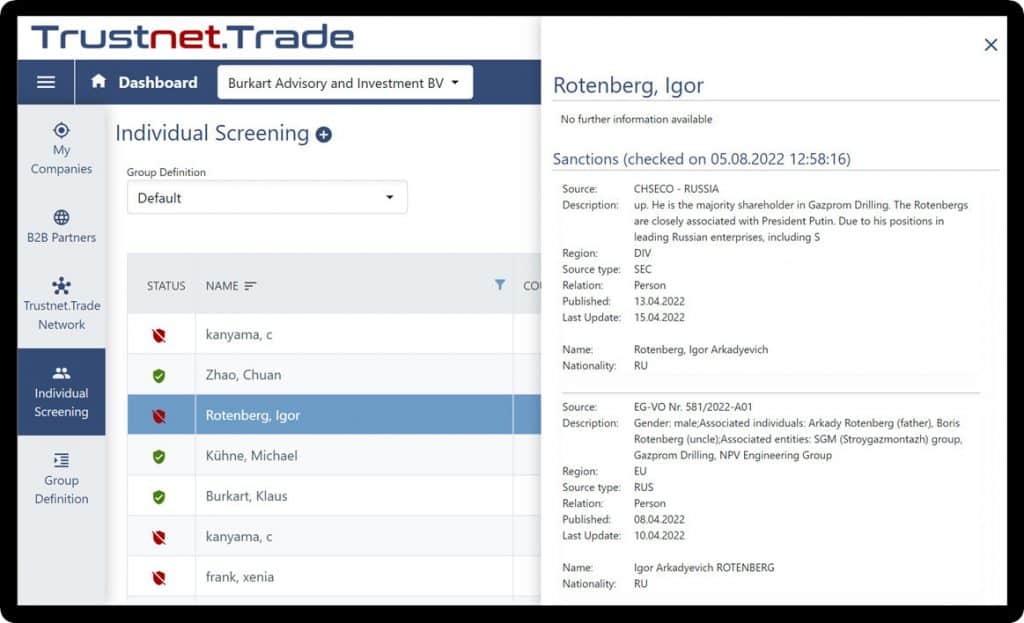

Trustnet.Trade führt eine umfassende Prüfung auf Sanktionen, Embargos, AMS, PEP für jedes identifizierte Unternehmen und jede Person (Ultimate Beneficial Owner, UBO) in der Eigentümerhierarchie Ihres Geschäftspartners durch.

Der KYB-Check entspricht den Vorschriften des deutschen, europäischen und des US-Geldwäschegesetzes.

Je nachdem, wie viele wirtschaftliche Eigentümer ermittelt wurden, dauert die Überprüfung zwischen 5 und 30 Sekunden.

Nach erfolgreicher Überprüfung kann ein Trustnet.Trade-Widget auf Ihre Website hochgeladen werden. Dieses Widget wird automatisch in Echtzeit aktualisiert. Es zeigt den Besuchern Ihrer Website deutlich Ihren proaktiven Ansatz und schafft Vertrauen.

Hinweise können über einen Link auf Ihrer Website personalisiert oder anonym angegeben werden. Eingehende Hinweise werden dann in der geschützten Umgebung von Trustnet.Trade bearbeitet und Ihre Mitarbeiter oder eine externe Stelle informiert.

Trustnet.Trade analysiert umfassend Datenquellen, um generische und spezifische Risiken für Länder und Geschäftspartner in einer Wertschöpfungskette zu erfassen. Risiken werden in einer Heatmap dargestellt. Durch Selbstauskünfte und Checks von lokalen Experten vor Ort können Risikoindikationen validiert werden.

Sollten durch die Risikoanalyse Risiken oder Verstöße identifiziert worden sein, werden im Risikomanagement angemessene Maßnahmen zugeordnet und verwaltet. Maßnahmen können kategorisiert und priorisiert, verantwortlichen Personen zugewiesen, Prüf- und Bearbeitungsaufträge erteilt und Termine überwacht werden.

Prüfungen werden durch unsere Partner Vor-Ort entweder über Desktop oder Live beim Lieferanten durchgeführt. Das Regelwerk dafür wird über Trustnet.Trade bereitgestellt.